WHAT BUDGET 2025 MEANS FOR YOU

WHAT BUDGET 2025 MEANS FOR YOU

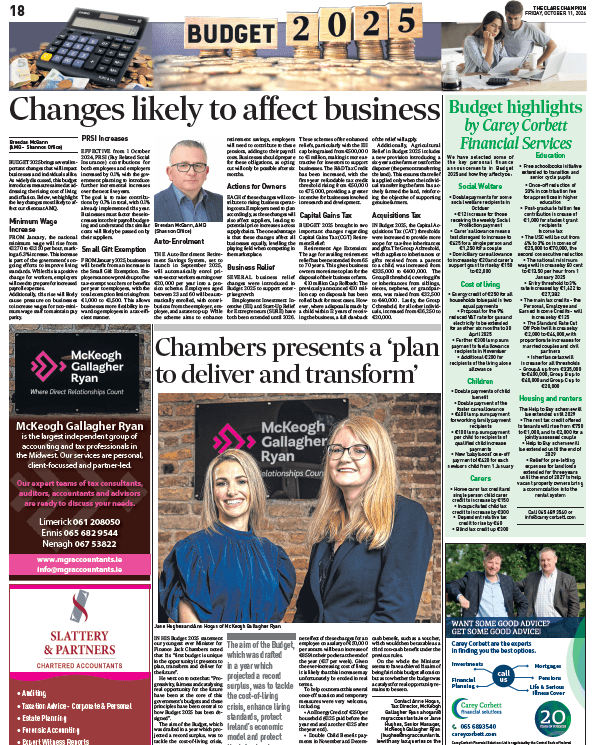

In his Budget 2025 statement our youngest ever Minister for Finance Jack Chambers noted that his “first budget is unique in the opportunity it presents to plan, transform and deliver for the future”. He went on to note that: “Progressivity, fairness and catalysing real opportunity for the future have been at the core of this government’s budgets and these principles have been central to how Budget 2025 has been designed”. The aim of the Budget, which was drafted in a year which projected a record surplus, was to tackle the cost-of-living crisis, enhance living standards, protect Ireland’s economic model and protect the infrastructure which attracts foreign investment.

With a surplus of €23.7billion, boosted by the windfall from Apple, the final budget was a €10.5billion package which aimed to provide a little something for everyone as opposed to providing any one large or specific tax break or incentive. The package was broken down into three core categories:

- €6.9billion of additional public spending.

- €1.4billion in taxation measure.

- €2.2billion once off cost-of-living measures.

Given the looming election Budget 2025 was, as expected, relatively fair to the individual taxpayer with the following changes to Income Tax and USC:

- A modest increase of €2,000 to the 20% tax band, the entry point to the 40% rate will be €44,000 for single individuals and €53,000 for married couples (with one earner).

- An increase to the ceiling of the 2% USC rate from €25,760 to €27,382 ensuring it remains the highest rate of USC paid by full-time minimum wage workers, when the National Minimum Wage increases on 1 January 2025 to €13.50.

- A decrease in the 4% rate of USC to 3%.

- All classes of PRSI will increase by 0.1 percentage point from 1 October 2024, followed by a further 0.1 percentage point in October 2025, gradually rising to 0.2 percentage points in October 2028.

- Increase of €125 to the Personal Tax Credit, Employee Tax Credit and Earned Income Tax Credit as well as corresponding increases to several other tax credits from the tax year 2025 onwards.

As an illustrative example, the net effect of these changes for an employee on a salary of €50,000 per annum will be an increase of €859 in their pocket at the end of the year (€17 per week). Given the ever-increasing cost of living it is likely that this increase may unfortunately be eroded in real terms.

To help counteract this several once-off taxation and temporary measures were very welcome, including:

- An Energy Credit of €250 per household (€125 paid before the year end and another €125 after the year end).

- Double Child Benefit payments in November and December 2024.

- The extension of the Help to Buy Scheme until the end of 2029.

- An increase in the Rent Tax Credit from €750 to €1,000 (€2,000 for a jointly assessed couple) for 2024 and 2025.

- Extension of the reduced 9% VAT rate on electricity and gas up to 30 April 2025. This VAT rate has also been extended to heat pump installations.

The €10,000 company car BIK reduction has been extended by one year, with confirmation that the provision of home car chargers by employers is exempt from BIK. Further welcome news is the increase in the annual Small Benefit Exemption from €1,000 to €1,500 which now allows an employer to provide up five non-cash benefits per year. This measure should provide clarity and comfort to employers who were concerned that the provision of small non-cash benefits, such as flowers and easter eggs, were fully utilising the Small Benefit Exemption before the employee received a larger non-cash benefit, such as a voucher, which would then be taxable as a third non-cash benefit under the previous rules.

Other positive measures for businesses include an increase in the first-year payment threshold for the Research & Development Tax Credit from €50,000 to €75,000 and the participation exemption for foreign dividends which, while not extended to branch income or non-treaty countries, should alleviate many time-consuming double tax relief computations. Class S PRSI (generally paid by owner-directors) can now be included in the calculations for Small Company Start-up Relief, which should see an increase in the number of start-ups eligible for Corporation Tax relief of up to €40,000, as the exclusion of Class S PRSI from the calculations resulted in a significant decrease in the relief available for small company start-ups in which the owners are also working directors.

There is good news for investors as Employment Investment Incentive (EII), Start-up Relief for Entrepreneurs (SURE) and Start-up Capital Incentive (SCI) are extended for a further two years to the end of 2026. The maximum amount on which an investor can claim relief for an EII investment has increased from €500,000 to €1,000,000 in one year for those lucky enough to have that level of cash available to invest and enough income taxable at 40% to utilise the relief. The limits applicable to Start Up Relief also increased from €700,000 to €980,000. Apart from making a pension investment, EIIS investment is the only option available to individuals trying to reduce their Income Tax bill and we are still finding that there is a huge appetite out there amongst individual taxpayers to make EIIS investments. The limit on Capital Gains Tax Investor ‘Angel’ Relief has also increased from €3million to €10million.

There were several key announcements on the property front, some of which were welcome and some surprising. Pre-letting expenses in respect of vacant residential premises have been extended to the end of 2027 as an incentive to owners of vacant property to bring accommodation into the rental market and clarification measures have been introduced in respect of the Residential Zoned Land Tax such that an exemption can be sought for land which is zoned residential but is used to carry out genuine economic activity such as farming for example. The Vacant Homes Tax will increase from five to seven times the property’s existing base Local Property Tax rate with the intent that the use of the existing housing stock will be maximised. The Stamp Duty rate applicable to multiple purchases of residential units has increased from 10% to 15% from midnight on 1 October, and in a surprise move, the Stamp Duty on high value residential property has increased such that the any purchase price (or market value where applicable) in excess of €1.5m is subject to Stamp Duty at a new rate of 6%. This new 6% rate effectively introduces a three-tiered stamping treatment for high value properties, with Stamp Duty levied at 1% on the first €1million, 2% on the next €500,000 and 6% on the excess. This ‘mansion tax’ is effective immediately with transitional measures to apply to binding contracts in place prior to 2 October 2024 where the instrument is executed before 1 January 2025. The government’s reasoning for this increase is that those who can afford to purchase a residential property with a purchase price of greater than €1.5million can also afford the increase in the Stamp Duty, however, time will tell the impact this will have on the sales of high value properties and the additional Stamp Duty yield.

Having been subject to fluctuation over the last few years, the Flat-rate Addition of VAT for farmers has increased from 4.8% to 5.1%. The Farmer’s Flat-rate Addition is paid to farmers who are not registered for VAT to compensate them for VAT paid on goods and services purchased in connection with their farming activities, so no doubt this increase will be welcome.

The VAT registration thresholds have also increased, effective from 1 January 2025. For suppliers of goods, the new threshold will be €85,000 (increased from €80,000) and for a supplier of services or mixed supplies, the threshold will be €42,500 (increased from €40,000). This is welcome news for small business who may have been approaching the VAT registration threshold and for whom a small breach of the threshold would create an administrative burden.

A very much anticipated and welcome increase in the Capital Acquisitions Tax thresholds is effective immediately, with the Group A threshold increasing from €335,000 to €400,000, Group B increasing from €32,500 to €40,000 and Group C increasing from €16,250 to €20,000. There has been no change to the rate which remains at 33% and the aggregation period remains the same, with all prior gifts and inheritance from 5 December 1991 to be aggregated when determining the remaining available Group threshold. The conditions from Agricultural Relief are also set to change with the announcement that the disponer (the person transferring the land) must also meet the active farmer test for a period of 6 years before the land is transferred. This new proposed condition is designed to narrow the application of Agricultural Relief to genuine active farmers and the next generation. We await the release of the Finance Act on 10 October 2024 to see how the test will be applied. The relief for Young Trained Farmers will be amended so that it will be available where it is claimed by an individual farmer who carries on the farm business through a company and agricultural stock reliefs have been extended to 31 December 2027.

Capital Gains Tax Retirement Relief which last year saw a cap of up to €10million introduced where the disponer is aged between 55 and 69 and the disposal is to a child (to come into effect on 1 January 2025) has seen a further change whereby the clawback period in respect of disposals to children in excess of €10million will be increased from 6 years to 12 years. We await the release of the Finance Act on 10 October 2024 to analyse the amended conditions for this relief in full but certainly there may be implications for the succession plans of many family businesses.

In a move that was not surprising, the Tobacco Products Tax increases the cost of a packet of cigarettes by €1, inclusive of VAT, effective from 2 October 2024. A tax on E-liquid products is to be introduced subject to a commencement order and will apply at a rate of €0.50 per millilitre.

On the whole the Minister seems to have achieved his aim of being fair in his budget allocation but as to whether the budget was a catalyst for real opportunity remains to be seen.

Please do not hesitate to contact Anne Hogan, Tax Director, McKeogh Gallagher Ryan ahogan@mgraccountants.ie or Jane Hughes, Senior Manager, McKeogh Gallagher Ryan jhughes@mgraccountants.ie with any tax queries on the Budget.

A condensed version of this article appeared in The Clare Champion on 11.10.2024.